Log in

Signup

Signup

Fairmat 1.7.0 offers new features and extensions as well several modelling improvements over the and 1.6.2 release.

-[Professional] New calibration procedure for equity modeling: we implemented a local volatility model following a global parametric approach proposed by Gatheral. This procedure allowed us to improve pricing accuracy in several scenarios. We want to thank Gerard Ascensi for helping us into this successful implementation.

-New and revised templates are available: Discount Certificates, Bonus Cap, Reverse Bonus Cap to mention some.

-Multi-Variate time-to-default can now be generated as a function of hazard rates. Handy when there is no credit information available about a given issuer.

-Added the possibility of setting a custom date in date transformation / advance. This helps in generating sequences of payments with non-standard schedules.

-Sensitivity and Impact analysis on arrays: with the new Fairmat version is possible to assess the impact of changes when elements are defined as vectors.

-New Functions are available: ALast (calculates the last index of an array satisfying a given condition), CumSum (calculates the cumulated sum of elements belonging to an array) and IssuerRecovery (calculates the recovery rate from a CDS ticker).

-Projects using Monte Carlo Simulation and Black can be mixed in the same project.

-The average operator now uses Monte Carlo simulation for averaging nodes instead of averaging expected values: this allows to preserve the information about the risk of subsequent nodes.

New Equity Templates

New Equity Templates

Market data provider selection

Market data provider selection

Exchange Rates Calibration Support

Exchange Rates Calibration Support

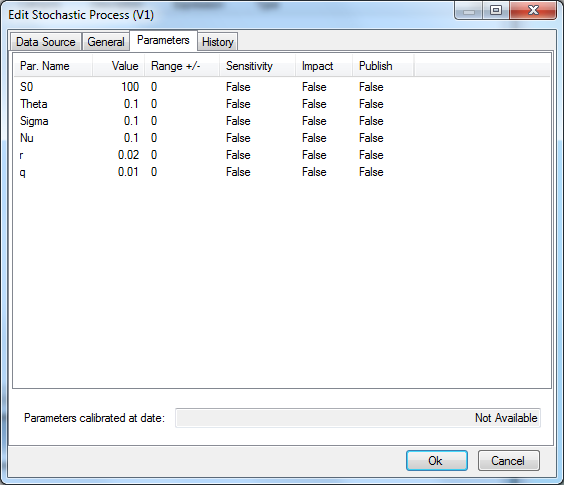

Variance-Gamma model in stochastic process

Variance-Gamma model in stochastic process

Variance-Gamma editing form

Variance-Gamma editing form